HOA management proposals have a presentation problem.

They arrive in professional packaging (bound documents, detailed service descriptions, testimonials, certifications) and they all make essentially the same promises. Responsive management. Transparent communication. Experienced staff. Competitive pricing. The board compares them against each other, usually on the basis of the monthly per-door fee, and selects the one that seems like the best value.

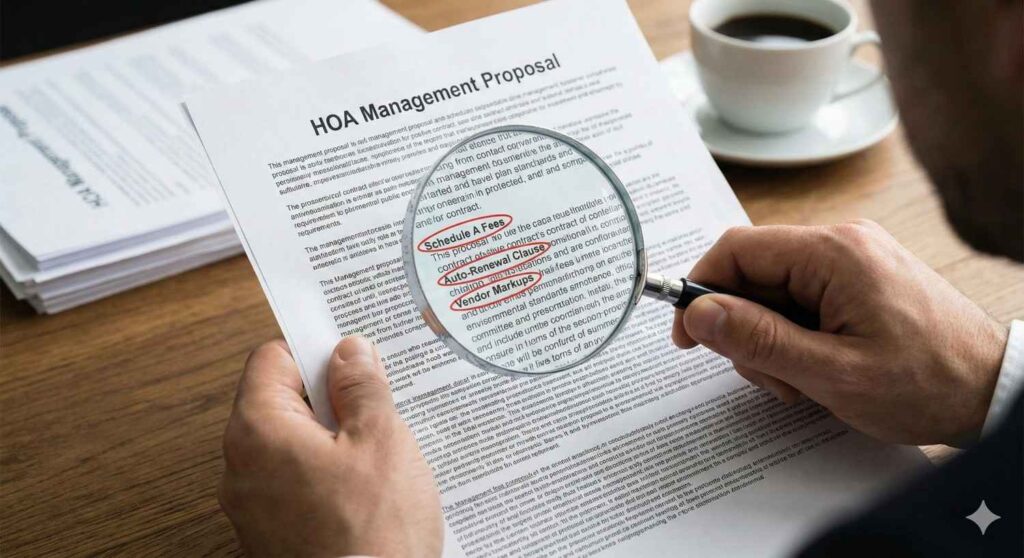

What most boards don’t realize until they’re twelve months into a contract is that the proposal’s front page is a marketing document, not a financial one. The actual cost of the management relationship (and the actual terms of it) lives in the appendices, the fee schedules, and the contract clauses that proposals are specifically designed to de-emphasize.

This guide covers six of the most consequential contract provisions and pricing practices that boards miss during the proposal evaluation process. Understanding them before you sign is significantly easier than addressing them after.

Trap 1: The Low Base Fee With a Hidden Fee Schedule

The base management fee (expressed as a monthly per-door charge) is the number that drives most proposal comparisons. A company that charges $12 per door per month appears more competitive than one charging $18, assuming all else is equal. The problem is that all else is rarely equal, and the base fee is rarely the total cost.

Most management company proposals include a schedule of fees (sometimes called Schedule A, Appendix A, or simply the fee schedule) that lists additional charges for specific services or transactions. This schedule is where companies that compete on a low base fee recover their margin: per-piece mailing fees, copying charges, after-hours call fees, board meeting attendance fees above a specified minimum, vendor invoice processing fees, resale certificate preparation fees, and similar per-transaction charges.

The practical impact depends on your community’s activity level, but for most active communities the ancillary fee load is significant. A community that generates high owner correspondence volume, has frequent vendor activity, and holds monthly board meetings may find that its effective management cost is 40% to 60% higher than the base fee suggests.

What to ask: request a complete schedule of every fee the company charges (not just the base fee) and ask for a sample year-end accounting from a comparable community showing actual total charges for the prior twelve months. The difference between the quoted base fee annualized and the actual total annual cost is the fee schedule impact.

Trap 2: The Financial Anchoring Tactic

Some management companies, during the proposal process, ask to see the association’s current budget or financial statements. The stated reason is usually something like “we want to understand your community’s needs” or “we need to see your financial health before we can quote accurately.”

In most cases the actual reason is simpler: they want to know what you’re currently paying so they can bid slightly below it. This is a negotiation technique called price anchoring: setting the baseline for what seems like a good deal based on what the buyer is already spending rather than on what the service is actually worth.

A management company that genuinely needs to understand the scope of work to build an accurate proposal can do so with publicly available information: property records, governing documents, a site visit, and a straightforward conversation about what the board needs. They don’t need your current budget to tell you what management should cost.

What to ask: if a company requests your current financials during the proposal process, ask them specifically what they need that information for and whether they can build a proposal without it. If they can’t explain a business reason that goes beyond understanding current pricing, that’s a useful signal about how they approach the relationship.

There is one exception worth noting: a request for the current reserve study is legitimate and useful. The reserve study tells a prospective management company what capital projects are coming, which informs how they staff and plan for the community. That’s a different request than asking to see your current management fee.

Trap 3: Vendor Markups and Referral Arrangements

Vendor management is one of the core services a management company provides: identifying qualified contractors, obtaining competitive bids, overseeing work, and processing invoices. When done well, this service saves the board significant time and produces better outcomes than boards trying to manage vendor relationships directly.

When done badly (or when structured around financial incentives that don’t align with the association’s interests), it costs the community money in ways that are difficult to detect.

The two most common misaligned incentive structures are invoice markups and vendor referral arrangements. Invoice markups involve the management company adding a percentage (typically 10% to 15%) to vendor invoices before passing them to the association. A $5,000 landscaping contract becomes a $5,500 or $5,750 charge. Referral arrangements involve vendors paying the management company a fee or percentage in exchange for being recommended to client communities, meaning the vendor’s pricing reflects the referral cost, and the management company has a financial incentive to steer business toward vendors who pay rather than vendors who deliver the best value.

Both arrangements are material conflicts of interest. A management company that profits from vendor invoices is not incentivized to negotiate aggressively on the community’s behalf. A company that receives referral payments from vendors is not acting as the association’s fiduciary when it selects those vendors.

What to ask: ask directly whether the company marks up vendor invoices and if so by what percentage. Ask whether the company receives any referral fees, commissions, or payments from vendors it recommends. Ask how vendors are selected and what the bidding process looks like. Request the underlying vendor invoices for a sample of transactions from a client community and compare them to what that community was charged.

Trap 4: Auto-Renewal and Restrictive Termination Clauses

Management contracts are typically multi-year agreements with specific termination provisions. The standard industry contract includes a one-year initial term with automatic annual renewal, meaning the contract renews for another year unless one party provides written notice of termination within a specified window before the renewal date.

The problem is in the details of that window. Some contracts require 90 days advance notice before the renewal date to prevent auto-renewal. If the board wants to exit at the end of year one but misses the 90-day notice window by a week, the contract automatically renews for another full year. The management company has no obligation to perform better during that year, and the board has no practical exit until the next renewal window opens.

Some contracts compound this with liquidated damages provisions: clauses that require the association to pay some portion of the remaining contract value if it terminates before the renewal date. A board that terminates for cause four months into a one-year term may owe eight months of management fees to a company it has already decided is not performing.

These provisions are not standard practice among all management companies. They are a choice, one that signals a company’s confidence (or lack thereof) in retaining clients through performance rather than contractual obligation.

What to ask: read the termination clause before signing anything. What notice is required to terminate, and when must that notice be given? Does the contract auto-renew, and if so what triggers renewal prevention? Are there any termination fees or liquidated damages provisions? What is the transition process when a contract ends? A management company that offers 30 to 60 days written notice for any reason with no termination fee is one that earns continued business through performance.

Trap 5: The Community-to-Manager Ratio

Management proposals typically promise a “dedicated community manager” or a “dedicated management team.” What the proposal rarely discloses is how many other communities that manager is simultaneously dedicated to.

A community manager responsible for 20 to 25 communities is managing too many to provide meaningful service to any of them. At that portfolio size, the manager is processing transactions (opening work orders, routing phone calls, generating financial reports), not actively managing community operations, building relationships with board members, conducting meaningful property inspections, or anticipating problems before they become emergencies.

The math is straightforward. A manager with 25 communities and a standard 40-hour work week has roughly 1.6 hours per community per week available before accounting for administrative overhead, meetings, and reactive tasks. That is not enough time to manage a community well.

Appropriate ratios depend on community size and complexity. Larger communities with active amenities, capital projects, and significant owner engagement warrant lower ratios. A manager carrying 8 to 12 larger communities can generally provide adequate service. Smaller, less active communities can support somewhat higher ratios. What matters is that the ratio is disclosed and that it reflects a realistic assessment of what the manager can do, not a number designed to sound reasonable during the proposal process.

What to ask: ask specifically how many communities the manager who would be assigned to your community currently manages. Ask what happens to your community’s management if that manager leaves: what is the transition protocol and how quickly is a replacement assigned? Ask what the company’s average manager tenure is, which is a proxy for how well the company treats its staff and how stable the management relationships it provides actually are.

Trap 6: Compliance Represented as a Value-Added Service

Some management companies present state law compliance (WUCIOA compliance in Washington, Davis-Stirling compliance in California) as a premium service requiring additional fees or specialized packages. The framing is that staying current with community association law is complex and that the board needs to pay extra for the company’s expertise in navigating it.

This framing has it backwards. WUCIOA and Davis-Stirling compliance is not an add-on to professional HOA management. It is a baseline requirement. A management company that manages Washington communities must be current on WUCIOA’s open meeting requirements (in effect since January 1, 2026), election administration requirements, reserve fund governance rules, and the full compliance framework that took effect for all communities by 2028. A management company that manages California communities must administer secret ballot elections correctly, follow the Davis-Stirling enforcement process, track SB 326 inspection deadlines, and prepare the required annual disclosures. These are not optional services.

A company that treats statutory compliance as a premium feature is either using it as a pretext for additional fees, or is signaling that its base service level doesn’t include what compliance actually requires.

What to ask: ask specifically how the company stays current on WUCIOA and Davis-Stirling developments. Ask how they updated their operations when SB 5796 amended WUCIOA in 2024. Ask them to walk you through how they administer a secret ballot election under Davis-Stirling. The answers will tell you quickly whether compliance is something they take seriously or something they use as a sales tool.

A Note on Comparing Proposals

The six items above share a common thread: they are all things that a well-structured proposal evaluation process would surface, but that a price-comparison approach will miss. The management company that wins on the lowest base fee is often not the management company with the lowest actual cost or the highest actual service level.

A better evaluation framework asks: what is the total cost of management, including all ancillary fees? What are the actual contract terms, including termination? Who specifically will manage this community, and what is their current portfolio? How does the company stay current on applicable state law? And can the company demonstrate its service quality through references from communities similar to ours, not references the company hand-selected, but a sample of current clients the board can contact directly?

Management company selection is one of the most consequential decisions an HOA board makes. The due diligence investment before signing is far less costly than the disruption of a management transition after discovering that the contract doesn’t reflect what the proposal implied.

How AmLo Management Approaches These Issues

AmLo Management’s pricing and contract terms are designed to be legible before you sign and consistent with what you expect after.

Our base fee is all-in. It covers the full scope of management services without a separate schedule of per-transaction charges. We do not mark up vendor invoices and do not receive referral fees from vendors we recommend. Vendor selection is based on quality, responsiveness, and price. Nothing else. We disclose our community-to-manager ratios before contracts are signed and assign specific named managers, not anonymous teams. Our termination terms are 60 days written notice for any reason with no termination fee.

On compliance: WUCIOA and Davis-Stirling compliance is part of what we do, not an add-on. We stay current on every legislative change (including the 2024 and 2025 WUCIOA amendments and California’s ongoing Davis-Stirling developments) and we update our operations and communicate changes to our clients as a matter of course.

If your board is evaluating management companies and wants a straightforward conversation about pricing, contract terms, and what management actually looks like in practice, contact AmLo Management. We’re happy to answer every question on this list, and to provide references from communities you can contact directly.

Disclaimer: This post is provided for general informational purposes only. HOA boards should review management contracts carefully and consult with qualified legal counsel before signing. Pricing practices, contract terms, and compliance obligations vary by company, market, and applicable state law.