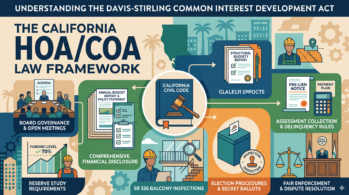

The Davis-Stirling Common Interest Development Act is the primary body of California law governing homeowners associations, condominium associations, and other common interest developments, codified at California Civil Code Sections 4000 through 6150 and setting board duties, member rights, governance procedures, financial-disclosure obligations, and enforcement mechanisms.

What Is the Davis-Stirling Common Interest Development Act?

The Davis-Stirling Common Interest Development Act is the primary body of California law governing homeowners associations, condominium associations, and other common interest developments.

First enacted in 1985 and significantly reorganized and recodified in 2014, the Davis-Stirling Act is codified in California Civil Code Sections 4000 through 6150 and establishes the legal framework for virtually every aspect of how a California HOA or COA operates.

The Act covers an extraordinarily broad range of association governance topics, from how a board is elected and how meetings must be conducted, to how assessments are collected, how disputes are resolved, and how the association’s finances must be disclosed to homeowners. For California HOA and COA boards, understanding the Davis-Stirling Act is essential. Violations of the Act can expose board members to personal liability, invalidate association actions, and create grounds for expensive litigation.

Unlike Washington’s Uniform Common Interest Ownership Act (WUCIOA), which is relatively modern and consolidated, the Davis-Stirling Act has accumulated decades of amendments, judicial interpretations, and companion legislation, including significant additions like SB 326 (2019), AB 3182 (2020), and AB 1101 (2021). Keeping up with California HOA law takes consistent attention, and most volunteer board members are already stretched thin.

Key Facts About the Davis-Stirling Act

What financial disclosures does Davis-Stirling require?

Davis-Stirling requires California HOAs to give every homeowner an annual disclosure package covering the budget, reserves, insurance, assessment-collection policy, and enforcement procedures, with specific delivery deadlines tied to fiscal-year-end under Civil Code Sections 5300 through 5320.

The Davis-Stirling Act imposes some of the most extensive HOA financial disclosure requirements in the country. California HOA boards are required to provide homeowners with a detailed annual disclosure package, commonly called the Annual Budget Report and Annual Policy Statement, that covers the association’s financial health, reserve fund status, planned expenditures, and key governance policies.

Annual Budget Report (Civil Code §5300)

The Annual Budget Report must be distributed to all members at least 30 to 90 days before the start of the association’s fiscal year. It must include the operating budget for the upcoming year, a reserve funding summary showing the current reserve balance and the percentage funded, a summary of the reserve study, and the estimated remaining useful life and replacement cost of major reserve components. The report must also disclose whether the board anticipates any special assessments in the coming year and explain the basis for any proposed assessment increases.

The reserve funding disclosure within the Annual Budget Report is one of the most scrutinized elements of California HOA governance – both by homeowners and by lenders and buyers who review it during real estate transactions. An association that is significantly underfunded relative to its reserve study raises immediate red flags for lenders and can directly impact a buyer’s ability to obtain financing for a unit purchase.

Annual Policy Statement (Civil Code §5310)

The Annual Policy Statement must be distributed within 30 to 90 days before the start of the fiscal year and must include the association’s collection and lien policies, enforcement and fine schedule, architectural review procedures, the location where association records are kept, and a summary of the dispute resolution process available to members. Beginning in 2022, the policy statement must also include a statement of the association’s policies regarding electric vehicle charging station installation rights.

Monthly and Annual Financial Statements

California HOAs are required to prepare and make available regular financial statements. For associations with gross revenues over $75,000 per year, a review of the annual financial statements by a licensed CPA is required every other year (unless the members vote to require an audit). Boards must also maintain financial records including ledgers, check registers, bank statements, and invoices for at least five years, and make these records available for member inspection upon request.

Financial Disclosure Checklist for California HOA Boards

Annual Budget Report distributed 30,90 days before fiscal year start

Annual Policy Statement distributed 30,90 days before fiscal year start

Reserve study updated – full study every 3 years, update study in alternate years

CPA review of annual financials (associations with gross revenues over $75,000)

Financial records maintained for minimum 5 years and available for member inspection

How does Davis-Stirling regulate assessment collection and delinquency?

Davis-Stirling requires California HOAs to follow a defined collection sequence: a written demand under Civil Code Section 5660, a pre-lien notice with a 30-day cure window, recording of an assessment lien, and only then a non-judicial or judicial foreclosure, with the board allowed to pursue civil suit at any point.

The Davis-Stirling Act establishes a detailed framework for HOA assessment collection and delinquency enforcement that California associations must follow precisely. Deviation from the statutory process, even when collection is clearly justified, can invalidate liens, expose the association to legal challenge, and result in the association bearing the cost of the homeowner’s attorney fees.

Pre-Lien Notice Requirements (Civil Code §5660)

Before recording a delinquency lien, the association must send a pre-lien notice to the delinquent owner at least 30 days before recording the lien. The notice must be delivered by first-class mail and certified mail, include the amount of the delinquency itemized by assessment, late charges, fees, and interest, and inform the owner of their right to request a payment plan and to dispute the debt through the association’s internal dispute resolution process. Failure to deliver proper pre-lien notice is one of the most common errors in California HOA collection enforcement and one of the most common grounds for lien challenges.

Payment Plans (Civil Code §5665)

California HOAs are required to offer delinquent homeowners a payment plan if requested. The payment plan must extend at least three months, and the association’s collection policy must describe the terms under which payment plans will be offered. Many associations are unaware of this obligation, which can create significant legal exposure when collection enforcement is challenged.

Assessment Increases and Special Assessments (Civil Code §5605, §5610)

Under the Davis-Stirling Act, the board may increase regular assessments by up to 20% per year above the previous year’s budget without member approval. Any increase exceeding 20% requires approval by a majority of a quorum of members. Special assessments that in aggregate exceed 5% of the association’s budgeted gross expenses for the fiscal year also require member approval. Boards that exceed these thresholds without proper member approval risk having the assessment invalidated.

What does Davis-Stirling require for HOA reserve funds?

Davis-Stirling requires every California common interest development association to commission a full reserve study at least every three years, update the study annually in the intervening years, and disclose the percent-funded ratio to members each year under Civil Code Sections 5550 through 5580.

California HOA reserve fund requirements under the Davis-Stirling Act are among the most detailed in the United States. The Act requires every California common interest development association to conduct a reserve study and maintain adequate reserve funding to cover the repair and replacement of major common area components.

Reserve Study Requirements (Civil Code §5550)

California HOAs must conduct a full reserve study – including a visual on-site inspection of all major common area components – at least every three years. In the intervening years, an update to the reserve study (without a new on-site inspection) must be completed. The reserve study must identify all major components with a remaining useful life of 30 years or less, estimate their remaining useful life and replacement cost, and calculate the annual contribution needed to maintain adequate funding. This calculation must be disclosed to members in the Annual Budget Report.

Reserve Funding Adequacy

The Davis-Stirling Act requires associations to annually determine and disclose to members the percentage of fully funded reserves – the ratio of the current reserve balance to the amount that would be in the reserve fund if it were ideally funded for all identified components at their current stage of useful life. While the Act does not mandate a specific minimum funding percentage, it does require disclosure of the current funding level and the association’s plan to achieve and maintain adequate funding. Associations that are less than 70% funded are considered underfunded by most reserve specialists and lenders.

In practice, inadequate reserve funding creates real pressure fast. When major components need replacement and the reserve fund is depleted, the association has two options: a special assessment – which can reach tens of thousands of dollars per unit in a condominium – or an association loan. Both options damage homeowner satisfaction, reduce property values, and reflect poorly on the board’s stewardship.

What does Davis-Stirling require for HOA board meetings?

Davis-Stirling requires California HOA boards to give members at least four days advance notice of every open board meeting, post the agenda in advance, conduct deliberations in open session except for the narrow executive-session topics defined by Civil Code Section 4935, and record decisions in minutes available to members on request.

California HOA board meetings are subject to strict transparency and notice requirements under the Davis-Stirling Act, far more extensive than most states. California boards operate under an “open meeting” standard that is functionally similar to requirements imposed on public agencies, though with certain exceptions for executive session topics.

Meeting Notice Requirements (Civil Code §4920)

Board meeting notices must be posted and distributed at least four days before the meeting. The notice must include the meeting agenda, and the board may generally only act on items included on the posted agenda. Emergency meetings may be called with less notice, but the definition of an emergency is narrow. Homeowners have the right to attend board meetings (with limited exceptions for executive session) and to speak during open forum before the board takes action on any agenda item.

Annual Meeting and Election Requirements

California HOA annual meetings and board elections are governed by extremely detailed procedural requirements under the Davis-Stirling Act and the California Corporations Code. Elections must be conducted by secret ballot using an inspector of elections. Notice of the election must be provided at least 30 days before ballots are distributed, and ballots must be available for counting for at least 30 days. Failure to follow the statutory election procedures precisely is one of the most common grounds for election challenges – and successful election challenges can invalidate an entire board election.

Executive Session

California boards may meet in executive session (without homeowners present) only for specific topics defined by statute – including litigation, contract negotiations, formation of disciplinary proceedings against a member, personnel matters, and a few others. The board must announce that it is going into executive session and the general subject matter. A common mistake is to conduct discussions in executive session that do not fall within the permitted topics – which can expose the board to challenge and liability.

What does SB 326 require for California condominium balcony inspections?

SB 326 requires every California condominium association with three or more units to commission a licensed-professional inspection of exterior balconies, decks, stairways, walkways, and their supports and railings by January 1, 2025 and every nine years thereafter, under Civil Code Section 5551.

Senate Bill 326 (2019), codified at Civil Code Section 5551, is one of the most significant additions to California HOA law in recent years and applies specifically to condominium associations. The statute names the items that must be inspected, the inspector qualifications, the inspection cycle, and the disclosure obligations to members.

What SB 326 Requires

SB 326 requires that the above-ground balconies, decks, stairways, walkways, and their supporting members be inspected by a licensed structural engineer or architect every nine years. The first round of SB 326 inspections was required to be completed by January 1, 2025 for associations with buildings in existence before 2020. The inspection must visually examine a statistically significant sample of the covered walking surfaces and their supports and report on their current condition, whether they are in a generally safe condition, and their expected useful life. If immediate safety hazards are identified, the association is required to take immediate corrective action and notify all residents.

SB 326 Compliance Deadlines

Many California condominium associations are still behind on SB 326, either because they were not aware of the requirement or because inspection scheduling was delayed. Non-compliance exposes boards to significant liability, particularly if a structural failure occurs on an element that should have been inspected. Associations that have not completed their initial SB 326 inspection should prioritize doing so immediately. AmLo coordinates SB 326 inspection scheduling and compliance tracking for all California condominium associations we manage.

SB 326 Quick Reference

How does Davis-Stirling regulate HOA rule enforcement?

Davis-Stirling requires California HOAs to follow a six-step rule enforcement sequence: adopt a fine schedule under Civil Code Section 5850, document the violation, send a written violation notice, give at least ten days notice of a disciplinary hearing under Section 5855, hold the hearing and issue a written decision within fifteen days, and offer Internal Dispute Resolution under Section 5915 before any lien or litigation.

For the full procedural sequence step by step, including how to document violations, draft a defensible violation notice, and run a Civil Code Section 5855 hearing, see How to Enforce HOA Rules Under the Davis-Stirling Act Without Getting Sued.

The Davis-Stirling Act establishes specific procedural requirements for how California HOA and COA boards enforce association rules and impose fines and penalties. Failure to follow the required disciplinary process is one of the most common grounds for homeowners to challenge fines and enforcement actions, and successful challenges can result in the association paying the homeowner’s attorney fees.

Pre-Hearing Notice and Right to Appeal (Civil Code §5850)

Before imposing a monetary penalty on a member for a violation of the association’s governing documents, the board must provide the member with written notice of the alleged violation and an opportunity to appear before the board at a hearing at least 10 days after the notice. The member has the right to appear with counsel, present evidence, and respond to the board’s allegations. The board must provide a written decision within 15 days of the hearing. A fine imposed without following this process is generally unenforceable.

Internal Dispute Resolution (Civil Code §5900)

The Davis-Stirling Act requires California HOAs to provide a fair, reasonable, and expeditious procedure for resolving disputes between members and the association. Before filing a civil lawsuit over most disputes, either the association or a member can request internal dispute resolution – an informal conference with a board member and the requesting party. Both parties are entitled to request this process and it must be completed within a reasonable time. Failure to respond to an IDR request can result in the association losing its ability to recover attorney fees.

When does a Davis-Stirling rule become unenforceable?

A rule is unenforceable when it fails one of the Civil Code Section 4350 validity tests, was adopted without the required member notice, or has been applied so inconsistently that a court treats it as waived. Section 4350 requires every operating rule to be in writing, within the board’s authority, consistent with the CC&Rs and California law, reasonable, and adopted in good faith. Selective enforcement, fining one owner for a violation the board ignores in others, is the most common way an otherwise valid rule becomes unenforceable in practice.

When a CC&R-based or rule-based restriction becomes unenforceable through selective enforcement, vague drafting, or conflict with a state or federal statute, the safest board response is to stop enforcing it, document why, and re-adopt a clean version under the Section 4360 procedure. For the full catalog of what makes a California HOA rule unenforceable and how to cure each defect, see Unenforceable HOA Rules: A California Board Guide.

What are the 2026 Davis-Stirling amendments?

The headline 2026 Davis-Stirling amendment is AB-130, which adds notice, hearing, and documentation requirements to the existing fine-enforcement sequence under Civil Code Sections 5850 through 5915.

Every California HOA and COA board operating in 2026 needs to assess whether its fine schedule, violation-notice templates, and disciplinary-hearing procedures still comply with the post-AB-130 procedural standard. Boards relying on a 2020-era fine schedule and 2020-era enforcement template are at the highest risk of a fine being invalidated under the new standard.

For the full AB-130 compliance walkthrough, including a side-by-side comparison of the pre-AB-130 and post-AB-130 fine cycles and a defensible fine-schedule template, see California AB-130 HOA Fines: A 2026 Board Compliance Guide.

Boards should also watch the 2026 California legislative calendar for follow-on bills affecting election procedures, reserve disclosure formatting, and rule-adoption notice requirements, which are routinely the subject of mid-decade Davis-Stirling housekeeping amendments.

Practically, AB-130 affects three operational documents every California HOA board should review before the next fine cycle: the recorded fine schedule (must reflect post-AB-130 procedural standards), the violation-notice template (must include the new content elements AB-130 requires), and the disciplinary-hearing minutes template (must capture the documentation required to defend the fine if challenged). A board that updates those three documents in early 2026 has done the substantive AB-130 compliance work; boards relying on pre-2026 templates carry rising enforcement-defeat risk every quarter the templates remain in use.

How has the Davis-Stirling Act been amended since 1985?

The Davis-Stirling Common Interest Development Act has been amended in nearly every California legislative session since its 1985 enactment.

Boards transitioning into the 2026 enforcement cycle need a clean view of how the statute has evolved, which amendments still drive operational requirements, and which legacy provisions have been superseded.

The timeline below summarizes the most operationally significant amendments. The 2014 SB 800 reorganization renumbered the entire statute from the pre-2014 Civil Code Sections 1350 through 1378 framework into the current Sections 4000 through 6150 structure; references in CC&Rs predating 2014 still point to the old section numbers and should be mapped during any governing-document update.

| Year | Bill | Section(s) affected | Summary |

|---|---|---|---|

| 1985 | Davis-Stirling Common Interest Development Act (original enactment) | Pre-2014 Civil Code §§1350 to 1378 | Established the original statutory framework for California common interest developments. |

| 2014 | SB 800 (effective date of 2014 reorganization) | Civil Code §§4000 to 6150 (renumbering) | Reorganized and recodified the entire Davis-Stirling Act into the current chapter and section structure. Substantive obligations largely carried forward; section numbers changed. |

| 2019 | SB 326 | Health and Safety Code (balcony inspection) | Required California condominium associations with three or more attached units to complete a balcony and structural walkway inspection by a licensed structural engineer or architect every nine years. First inspection deadline: January 1, 2025. |

| 2020 | AB 3182 | Civil Code §4741 | Limited the extent to which HOA governing documents may restrict rentals; established a 25% cap on rental prohibitions and required associations to permit short-term and long-term rentals subject to reasonable governance rules. |

| 2021 | AB 1101 | Civil Code §5380, §5502 and related financial-control provisions | Strengthened financial control requirements for HOAs, including signature and authorization rules for transfers out of operating and reserve accounts; reinforced fidelity-bond and fiduciary protections. |

| 2026 | AB-130 | Civil Code §5855 and supporting fine-enforcement provisions | Amended Davis-Stirling fine-enforcement procedures to require additional notice, hearing, and documentation before assessing or collecting a monetary penalty against a homeowner. See the California AB-130 HOA Fines guide for the dedicated walkthrough. |

| 1994 | AB 314 (Reorganization) | TBD section | Reorganized record-keeping and member-inspection rights ahead of the broader 2014 recodification. |

| 2003 | SB 137 (Election Reform) | TBD section | Established statutory secret-ballot procedures and the inspector-of-elections role for HOA elections. |

| 2005 | AB 1098 (Open Meeting Act expansion) | TBD section | Extended the Common Interest Development Open Meeting Act notice and executive-session restrictions to most board actions. |

| 2012 | SB 563 (Email and Online Voting) | TBD section | Authorized electronic delivery of certain notices and member-approved online voting procedures. |

| 2016 | SB 407 (Service Members) | TBD section | Added notice and rate protections for assessments owed by deployed service members. |

| 2017 | AB 1412 (Director Personal Liability) | TBD section | Clarified the standard for board-member personal liability in volunteer-director contexts. |

| 2018 | AB 2912 (Financial Controls) | TBD section | Imposed monthly bank-statement review and reserve-transfer ratification requirements on California HOA boards. |

| 2022 | AB 1410 (Pandemic-Era Enforcement) | TBD section | Limited fine-imposition for governing-document violations tied to pandemic-related missed assessments. |

| 2023 | SB 392 (Voting Procedures) | TBD section | Clarified electronic and proxy voting standards introduced under SB 563 and AB 502. |

| 2024 | AB 1764 (Records Inspection) | TBD section | Tightened response timelines and copy-fee caps for member document-inspection requests. |

The amendments listed above are the most operationally significant for board governance. Other Davis-Stirling amendments have addressed election procedure, member voting, ADU rights, electric vehicle charging stations, drought-tolerant landscaping, and pet rules. Boards updating governing documents should commission a current statutory review with counsel rather than relying on any single timeline.

How is the Davis-Stirling Act organized in the California Civil Code?

The post-2014 Davis-Stirling Act is organized into eleven chapters spanning California Civil Code Sections 4000 through 6150, with each chapter grouping a defined set of governance obligations.

The index below shows the chapter structure with the operational topics each chapter addresses. Boards working a specific compliance question (a fine, a reserve study, a member-records request) can use the index to jump to the right statutory neighborhood.

| Civil Code chapter | Sections | Topic |

|---|---|---|

| Chapter 1: General Provisions | §§4000 to 4200 | Definitions, applicability, common interest development types, governing-document hierarchy. |

| Chapter 2: Application of Act | §§4201 to 4275 | Statutory applicability rules, federal preemption boundaries, application to mixed-use developments. |

| Chapter 3: Governing Documents | §§4250 to 4370 | CC&Rs, bylaws, rule adoption procedure, recorded-document hierarchy, amendment standards. Section 4350 sets the validity tests an operating rule must pass to be enforceable; see Unenforceable HOA Rules. |

| Chapter 4: Ownership and Transfer | §§4500 to 4790 | Ownership interests, common-area rights, transfer disclosures, escrow obligations, lender requirements. |

| Chapter 5: Property Use and Maintenance | §§4700 to 4790 | Use restrictions, architectural review, drought-tolerant landscaping, ADUs, electric vehicle charging, solar drying, flag display. |

| Chapter 6: Association Governance | §§4900 to 5260 | Board powers, member meetings, open-meeting requirements, elections and voting, executive session, member-records access. |

| Chapter 7: Finances | §§5300 to 5580 | Annual budget report, annual policy statement, reserve studies, reserve-funding policy, financial controls. See How to Build an HOA Budget That Actually Works for the operational walkthrough. |

| Chapter 8: Assessments and Collection | §§5600 to 5740 | Regular and special assessments, member-vote thresholds, pre-lien notice, lien recording, judicial and non-judicial foreclosure. See HOA Special Assessments for the member-approval thresholds and procedural sequence in plain English. |

| Chapter 9: Insurance | §§5800 to 5810 | Master property and liability insurance requirements, directors-and-officers coverage, insurance disclosures. |

| Chapter 10: Discipline and Dispute Resolution | §§5850 to 5985 | Fine schedule and fine-enforcement procedure (§5855), monetary-penalty limits (§5725), Internal Dispute Resolution (§§5910 to 5919), Alternative Dispute Resolution (§§5925 to 5965), attorney's fees (§5975). See How to Enforce HOA Rules Under Davis-Stirling for the procedural deep dive, and AB-130 California HOA Fines for the 2026 fine-enforcement amendment. |

| Chapter 11: Construction Defect Litigation | §§6000 to 6150 | Pre-litigation procedure for construction defect claims, builder notice and right-to-cure provisions. |

The chapter structure matters operationally because Davis-Stirling questions almost always live within one chapter at a time. A fine schedule question lives in Chapter 10; a reserve study question lives in Chapter 7; a board-meeting notice question lives in Chapter 6. Boards that map their compliance calendar to the chapter structure (one chapter per quarter for review, with Chapter 7 and Chapter 8 reviewed annually because of their fiscal-year tie) consistently catch procedural drift before it produces a homeowner challenge.

California associations that retain professional management benefit from a manager who can route each board question to the correct chapter on first reading. AMLO serves California HOA and COA boards with a compliance workflow built around the Davis-Stirling chapter structure, so boards never have to remember whether the question they are asking lives in Chapter 6, 7, or 10.

Chapter boundaries and section ranges reflect the post-2014 reorganization. Specific section numbers within each chapter may shift as the statute is amended; cite to the current published California Civil Code when relying on a specific section number for policy work.

How do California HOAs amend CC&Rs and operating rules under Davis-Stirling?

California HOAs amend recorded CC&Rs by securing the member-approval percentage stated in the declaration and recording the amendment with the county recorder, while operating rules change through a shorter board-adopted procedure under Civil Code Section 4360 that requires a 28-day member comment period before the rule takes effect.

The two document types follow different paths because they sit at different levels of the governing-document hierarchy. CC&Rs are recorded restrictions that bind the land and require a member vote to change. Operating rules are board decisions that implement the CC&Rs and can be adopted or repealed by the board alone, subject to notice.

How do you amend recorded CC&Rs?

Under Civil Code Section 4270, a CC&R amendment becomes effective once the association obtains the approval percentage the declaration requires, commonly between 51 percent and 75 percent of the total voting power, and records the amendment. When a board cannot reach the required supermajority despite a good-faith vote, Civil Code Section 4275 lets the association petition the superior court to approve the amendment at a lower threshold, provided more than 50 percent of those voting approved it and turnout met the statutory minimum. The Section 4275 court petition is the standard remedy for HOAs whose 1980s declarations set amendment thresholds so high they are effectively unamendable.

How do you adopt or change an operating rule?

Civil Code Section 4360 requires the board to give members written notice of a proposed operating-rule change at least 28 days before adopting it, with the text of the change and its purpose. The board then adopts the rule at an open meeting. Under Civil Code Section 4365, members holding 5 percent of the voting power can call a special vote to reverse a board-adopted rule within a set window, which is the member check on unilateral rule changes.

Both paths feed back into enforceability. A CC&R amendment recorded without the required vote, or an operating rule adopted without the Section 4360 notice, is open to challenge. Boards weighing a CC&R amendment should start with how the documents rank; see our guide to what CC&Rs are and how they sit in the governing-documents hierarchy. For the validity tests an operating rule must satisfy and the defects that void one, see Unenforceable HOA Rules: A California Board Guide.

What are the Davis-Stirling election and voting requirements?

Davis-Stirling requires California HOAs to elect directors by secret double-envelope ballot under Civil Code Sections 5100 through 5145, to adopt election operating rules in advance of an election, and to appoint an independent inspector of elections who is not a current director, a candidate, or related to one.

The current election regime took its modern shape with SB 323, effective January 1, 2020, which tightened candidate-qualification limits, expanded the secret-ballot requirement, and added member access to election records. Boards still running elections on pre-2020 procedures are the most exposed to a challenge.

Which decisions require a secret ballot?

Civil Code Section 5100 requires a secret double-envelope ballot for elections of directors, assessments that need member approval, amendments to the governing documents, and grants of exclusive use of common area. The double-envelope method, an unmarked inner ballot inside a signed outer envelope, separates the vote from the voter so the inspector can verify eligibility without seeing how anyone voted.

What does the inspector of elections do?

Under Civil Code Sections 5110 and 5120, the inspector of elections receives the ballots, verifies member eligibility, counts the votes in public at an open meeting, and takes custody of the ballots afterward. The inspector must be independent of the board and the candidates. Counting ballots outside an open meeting, or letting a sitting director tally the votes, is a frequent and easily challenged election defect.

What are the election operating rules?

Civil Code Section 5105 requires associations to adopt election operating rules covering candidate qualifications, nomination procedures, voting methods, and the use of association media and common areas during a campaign. These rules cannot be amended within the 90 days before an election. A member who proves an election-law violation can ask a court to void the result and recover civil penalties of up to 500 dollars per violation under Civil Code Section 5145.

What records can California HOA members inspect under Davis-Stirling?

Davis-Stirling gives California HOA members the right to inspect and copy association records under Civil Code Sections 5200 through 5240, with current-year records due within 10 business days of a written request and records from the prior two fiscal years due within 30 calendar days.

The statute splits records into two tiers. Standard association records include budgets, financial statements, board-meeting minutes, membership lists, and contracts. Enhanced association records, which include check registers and individual ledgers, carry tighter access conditions because they touch individual financial detail.

Civil Code Section 5210 sets the response deadlines by record age, and Section 5215 lets the association redact specified private information, such as another member’s contact details or disciplinary records, before producing records. A board cannot use redaction as a pretext to withhold a record a member is entitled to see.

When a board ignores or stonewalls a proper records request, Civil Code Section 5235 lets the member sue to compel production and recover a civil penalty of up to 500 dollars for each denial, plus costs. Records disputes are among the most common reasons California boards end up in litigation with their own members, and almost all are avoidable with a written records-request log and a standard response timeline.

What are the common Davis-Stirling Act misspellings and abbreviations?

The Davis-Stirling Act is one of the most commonly misspelled and abbreviated statute names in California real estate law, with searchers landing here under at least eight written variants of the same statutory body.

The misspellings, prefix variants, and abbreviations below all refer to the same body of law: California Civil Code Sections 4000 through 6150. If you arrived at this guide by searching for any of these variants, you are in the right place.

Is it "Davis-Stirling" or "Davis Sterling"?

The correct spelling is Davis-Stirling. The Act is named for its 1985 legislative sponsors, Senator Lawrence W. Stirling and Assemblymember Mike Davis. "Stirling" is the surname; "Sterling" is a common misspelling that does not appear in the official California Civil Code citation.

What is the "Davis Sterling Act" or "David Sterling Act"?

These are misspellings of the Davis-Stirling Common Interest Development Act. There is no separate "Davis Sterling Act" or "David Sterling Act" in California law. Search engines and HOA discussion forums frequently surface these variants, but they refer to the same statute codified at Civil Code Sections 4000 through 6150.

Is "Stirling Davis Act" a thing?

No. The Act is consistently referred to as the "Davis-Stirling Act," "Davis-Stirling Common Interest Development Act," or simply "Davis-Stirling." Reversing the names to "Stirling Davis" does not produce a separate statutory framework; it produces another search-engine variant of the same underlying body of law.

Why do California HOAs care about the spelling?

Board members and homeowners who search for "Davis Sterling Act" or one of its variants are looking for guidance on the same statute that AMLO's board members work with every day. AMLO's published guidance on Davis-Stirling rule enforcement, reserve studies, balcony inspections, financial disclosure, and the 2026 AB-130 amendment all apply regardless of how a member happens to search for the underlying statute name.

Is “CA Davis Stirling” or “California Davis Stirling” a different statute?

No. “CA Davis Stirling,” “California Davis Stirling,” and “ca davis stirling” are all common state-prefix shorthand referring to the same California Davis-Stirling Common Interest Development Act at Civil Code Sections 4000 through 6150. There is no separate “CA Davis-Stirling” statute; the Act only exists in California, so the state-prefix is technically redundant but appears frequently in board-member search queries.

What is the “DS Act” or “DSCRA” abbreviation?

“DS Act” is a common informal abbreviation for the Davis-Stirling Act used in board emails and management-company correspondence. “DSCRA” is a less standard abbreviation sometimes used by California attorneys to stand for “Davis-Stirling Common Interest Development Act.” Both refer to the same statute codified at Civil Code Sections 4000 through 6150. AMLO uses the unabbreviated form in formal documentation to avoid confusion with the federal Servicemembers Civil Relief Act (SCRA).

Is “California Common Interest Development Act” the same as Davis-Stirling?

Yes. The Act has two names: the “Davis-Stirling Common Interest Development Act” (the formal statutory name honoring the 1985 sponsors) and the “California Common Interest Development Act” (the substantive subject-area name describing what the statute covers). Both names refer to the same body of law at Civil Code Sections 4000 through 6150. Legal-academic and policy writing tends to prefer “Common Interest Development Act”; practitioner and board-facing writing tends to prefer “Davis-Stirling.”

What is the “Davis-Stirling Act 2024” or “Davis-Stirling Act 2026” version?

There is no separate “2024 version” or “2026 version” of the Davis-Stirling Act. The Act is a single statute that the California Legislature amends in nearly every legislative session. “Davis-Stirling Act 2024” usually refers to the statute as amended by the bills enacted during the 2023-2024 legislative session, and “Davis-Stirling Act 2026” refers to the statute as amended through the 2025-2026 session (which includes AB-130, the 2026 headline amendment). For the running list of session-by-session amendments, see the amendments timeline section above.

What are the key Davis-Stirling reference points for California boards?

Most Davis-Stirling questions a California board faces ultimately point to a specific Civil Code section, a particular legislative session amendment, or one of the named subordinate frameworks like the Open Meeting Act.

The reference subsections below address the long-tail questions California board members search most often.

What is a common interest development under California law?

A common interest development (CID) under California law is a residential community in which owners hold both an individual interest in their lot or unit and an undivided interest in common areas, governed by recorded CC&Rs and a homeowners or community association.

Civil Code §4100 defines CIDs to include condominium projects, planned developments, stock cooperatives, and community apartment projects. Each form has its own ownership mechanics, but the Davis-Stirling Act governs all of them through a single body of law. Boards sometimes assume their community is exempt because the term “HOA” doesn’t appear on the recorded documents; it almost never is.

What is the difference between Davis-Stirling and the Common Interest Development Act?

There is no substantive difference. “Davis-Stirling Act” and “Common Interest Development Act” are two names for the same body of California law, codified at Civil Code §§4000 through 6150.

“Davis-Stirling” refers to the 1985 sponsors of the original legislation. “Common Interest Development Act” is the formal Civil Code title used by the legislature. California practitioners use both names interchangeably. Older treatises and CC&R amendments tend to use “Davis-Stirling,” while statute citations in newer legal databases use the formal title. Either name points to the same statute.

Where is the Davis-Stirling Act in the California Civil Code?

The Davis-Stirling Act is codified at California Civil Code §§4000 through 6150, organized into chapters covering definitions, governance, finances, transfer disclosures, common area maintenance, dispute resolution, and miscellaneous provisions.

The chapter index below reflects the post-2014 reorganization that consolidated the prior §§1350-1378 framework into the current numbering. Verify the current chapter boundaries against leginfo.legislature.ca.gov before citing in policy or governing documents.

| Civil Code range | Topic |

|---|---|

| §§4000-4275 | General provisions, definitions, governing documents |

| §§4340-4370 | Application of governing documents and rule adoption |

| §§4500-4895 | Common area, operations, board powers and elections |

| §§4900-4955 | Open Meeting Act (board meetings, notice, executive session) |

| §§5000-5320 | Financial reports, budgets, annual disclosures |

| §§5500-5580 | Reserve studies and reserve funding |

| §§5600-5740 | Assessments, liens, foreclosure, payment plans |

| §§5800-5965 | Discipline, dispute resolution, enforcement, IDR/ADR |

| §§6000-6150 | Miscellaneous and transitional provisions |

What happened to Civil Code §1365 after the 2014 reorganization?

Civil Code §1365 was the pre-2014 budget-disclosure section of the Davis-Stirling Act. The 2014 reorganization split its substance across three new sections: the annual budget report at §5300, the year-end financial summary at §5305, and the annual policy statement at §5310.

If your CC&Rs or operating rules still cite §1365, the citation is not invalid; it simply references the pre-2014 version of the statute. The substantive obligations have carried forward in nearly every case, but the section numbers have changed. Boards updating governing documents should map the legacy citations to current sections. The translation table below covers the most common pre-2014 citations boards still encounter.

| Pre-2014 citation | 2014+ citation | Topic |

|---|---|---|

| §1363 | §§4900-4955 | Open Meeting Act / board meetings |

| §1365 | §5300 | Annual budget report |

| §1365(a)(2) | §5310 | Annual policy statement |

| §1365.1 | §5705 | Pre-lien assessment notice |

| §1365.2 | §5200 | Member document inspection |

| §1366 | §5605 | Assessment increases |

| §1367.1 | §§5650-5660 | Assessment liens and foreclosure |

| §1369.510 | §5900 | Internal Dispute Resolution (IDR) |

| §1378 | §4765 | Architectural review |

What is the Davis-Stirling Open Meeting Act?

The Davis-Stirling Open Meeting Act is the common name for Civil Code §§4900 through 4955, the chapter of the Act that defines what constitutes a board meeting, requires advance notice to members, limits the use of executive session, and protects the member’s right to attend and observe.

Civil Code §4925 defines a “board meeting” broadly: any congregation of a quorum of directors at the same time and place to hear, discuss, or deliberate on association business. Email exchanges among directors that constitute deliberation can satisfy the definition and trigger notice and minutes obligations, which is the most common compliance trap for self-managed boards. Section 4920 sets a four-day general meeting notice (electronic delivery permitted) and a two-day standard for emergency meetings. Section 4935 enumerates the narrow set of topics that may be discussed in executive session: pending or potential litigation, member discipline, personnel decisions, contract negotiation, and assessment delinquency. Anything outside that list belongs on the open agenda.

What 2024 amendments did the Davis-Stirling Act include?

The 2024 California legislative session produced a set of Davis-Stirling amendments addressing electronic voting, member communications, and disclosure timing. Specific bill numbers and effective dates change with each session and should be confirmed against the current statute on leginfo.legislature.ca.gov before being relied on for policy.

The pattern is consistent across recent sessions: the legislature continues to refine the procedural baseline that protects member rights (notice, disclosure, voting access) while gradually expanding the digital-first delivery options available to boards. Boards rebuilding their election procedures, document delivery practices, or assessment workflows should treat the statute as a moving target and revisit each cycle. The 2025 and 2026 amendments below build on this same trajectory.

What 2025 and 2026 amendments to the Davis-Stirling Act apply now?

The most consequential 2026 amendment to the Davis-Stirling Act is AB-130, which tightens fine-enforcement procedures for HOAs by adding notice, hearing, and documentation requirements before a board may assess or collect a monetary penalty. Other recent amendments have continued refining electronic voting rules, balcony inspection deadlines under SB 326, and document inspection standards.

AB-130’s procedural changes affect every California HOA that levies monetary penalties. Boards should rebuild fine schedules, violation-notice templates, and hearing procedures to meet the new requirements before assessing fines in 2026. AMLO has published a dedicated practitioner guide to AB-130’s enforcement procedures covering the seven-step compliant fine cycle, the post-AB-130 fine schedule checklist, and the consequences of procedural failure.

How does AMLO support California boards on Davis-Stirling compliance?

AMLO Community Management runs Davis-Stirling compliance as a year-round operational discipline for California HOA and COA boards, covering the annual disclosure calendar, reserve-study scheduling, board-meeting notice cadence, fine-schedule administration, and SB 326 inspection tracking.

The Davis-Stirling Act’s detailed requirements create a significant ongoing compliance burden for California HOA and COA boards. The financial disclosure obligations alone require careful calendar management, professional-grade financial reporting, and coordination with reserve study specialists and CPAs. Add board meeting procedures, election administration, enforcement protocols, and SB 326 compliance tracking – and the scope of what a California HOA board must manage correctly becomes genuinely demanding for volunteers.

A management company with real Davis-Stirling expertise is more than a convenience – for many California associations, it is the difference between staying compliant and taking on avoidable risk. The right management company does more than process work orders and collect assessments. It understands the statutory calendar, prepares the required annual disclosures, administers elections under proper Civil Code procedures, tracks SB 326 inspection deadlines, manages the delinquency process correctly, and keeps the board informed of upcoming legal obligations.

AmLo Management provides full-service HOA and COA management for communities across Los Angeles and Ventura counties with deep Davis-Stirling compliance expertise. Our Marina del Rey office serves communities throughout the greater Los Angeles area – from Simi Valley and Thousand Oaks to Santa Clarita, Marina del Rey, and surrounding communities.

HOA Management

Full-service Davis-Stirling compliant management for single-family HOAs, townhome communities, and master planned developments across Los Angeles and Ventura counties.

COA Management

Condominium association management with SB 326 compliance coordination, complex capital planning, and Davis-Stirling expertise across Los Angeles and Ventura counties.

For California HOA boards considering a management transition or evaluating Davis-Stirling compliance gaps in current operations, AMLO offers a structured intake call that walks the board through the chapter-by-chapter compliance review. The conversation typically surfaces one or two procedural items that an outgoing or self-managing operation has been handling out of alignment with the post-2014 statute, which boards can then prioritize for resolution before they become enforcement exposures.

AMLO serves California HOA and COA boards across the state, with deep concentrations in the Los Angeles metro and Greater Los Angeles area. Boards in Los Angeles County, Ventura County, and the surrounding region work with the same Davis-Stirling specialist team that handles the rest of the AMLO California portfolio, with the operational benefit of a local manager familiar with regional vendor networks and county-level compliance nuances.